Linkages between account establishment routines and overseas remittance barriers in web commerce systems

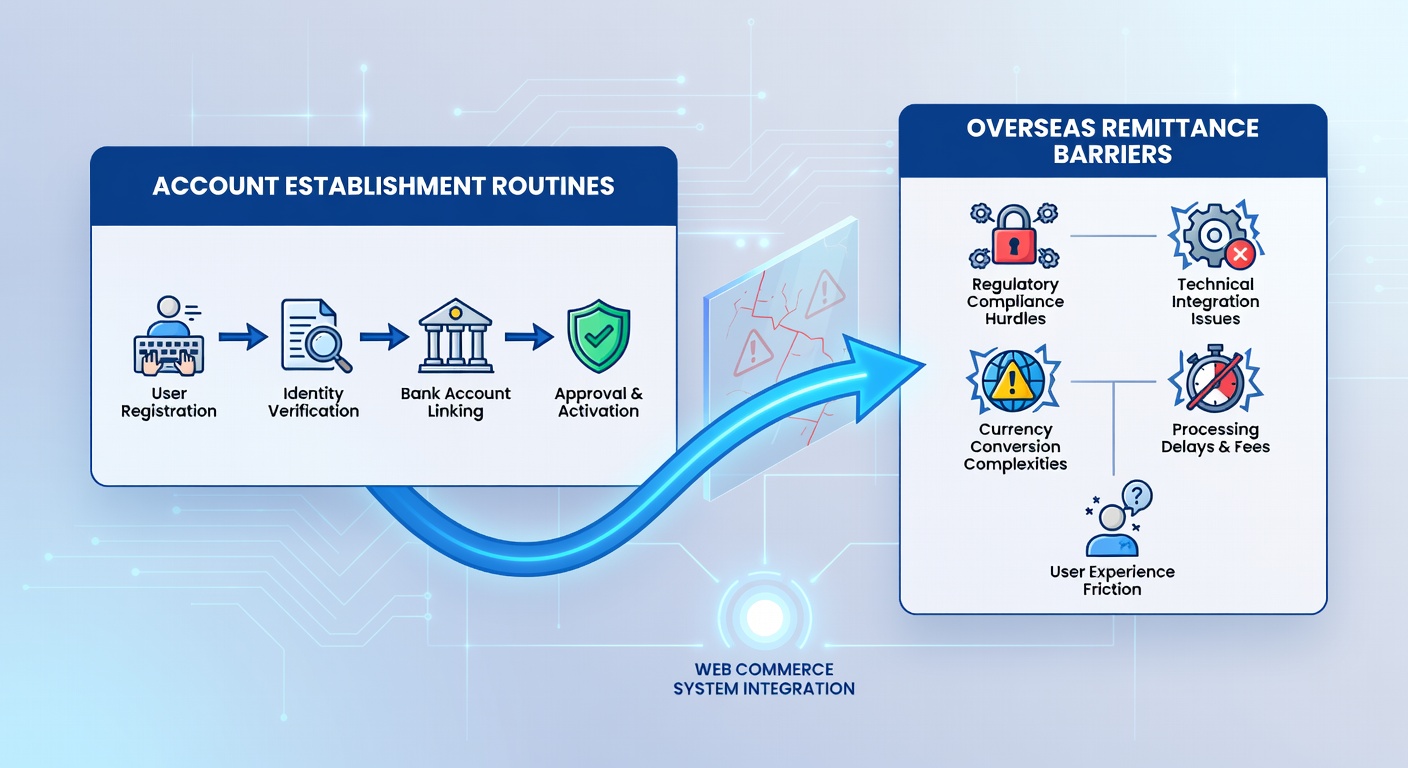

Account establishment routines in web commerce systems often determine how smoothly overseas remittances reach merchants and service providers. These routines involve identity verification, compliance checks, and integration with payment gateways. Data from global transaction networks shows that delays during account creation directly affect remittance timelines across borders. Researchers at institutions tracking cross-border payments note that incomplete verification steps create bottlenecks when funds originate from multiple jurisdictions. Many platforms require users to submit documentation before activating merchant accounts. This process aligns with anti-money laundering standards enforced by regulatory bodies in different regions. Observers note that variations in these requirements between countries lead to inconsistent remittance processing speeds. In June 2026, updates to verification protocols in several markets highlighted ongoing coordination challenges between account setup and fund movement.

Account establishment routines in web commerce systems often determine how smoothly overseas remittances reach merchants and service providers. These routines involve identity verification, compliance checks, and integration with payment gateways. Data from global transaction networks shows that delays during account creation directly affect remittance timelines across borders. Researchers at institutions tracking cross-border payments note that incomplete verification steps create bottlenecks when funds originate from multiple jurisdictions. Many platforms require users to submit documentation before activating merchant accounts. This process aligns with anti-money laundering standards enforced by regulatory bodies in different regions. Observers note that variations in these requirements between countries lead to inconsistent remittance processing speeds. In June 2026, updates to verification protocols in several markets highlighted ongoing coordination challenges between account setup and fund movement.Core Elements of Account Establishment

Web commerce platforms typically follow structured sequences for account creation. These sequences include email confirmation, business registration details, and bank account linkage. Studies from payment industry analysts indicate that streamlined sequences reduce friction for international users. Yet longer verification chains appear when platforms operate across multiple regulatory environments.

Compliance layers add another dimension. Platforms integrate checks against sanctioned lists and perform risk assessments. Those who've examined transaction data observe that high-risk jurisdictions trigger additional reviews during account setup. This extra scrutiny often extends the time before remittances can flow without interruption.

Overseas Remittance Barriers

Remittance barriers emerge from currency conversion limits, intermediary bank fees, and regulatory caps on transfer amounts. Reports compiled by organizations monitoring global finance show these barriers intensify when sender and recipient accounts sit in different compliance frameworks. Currency controls in certain economies create further hurdles for web-based merchants receiving payments from abroad.

Technical mismatches between payment rails compound the issue. Some systems rely on SWIFT messaging while others use real-time rails with different data requirements. Figures from transaction monitoring services reveal that these mismatches account for a measurable share of failed or delayed remittances in e-commerce channels.

Direct Linkages and Interaction Points

Account establishment routines intersect with remittance barriers at several key points. Verification delays during onboarding postpone the activation of remittance channels. Once accounts activate, mismatched documentation formats between regions can still halt transfers mid-process. Analysts tracking these patterns find that early resolution of verification gaps correlates with fewer subsequent remittance interruptions.

What's interesting is how shared data fields create ripple effects. Information collected during account setup such as tax identification numbers and address proofs feeds directly into remittance compliance checks. When these fields fail to match across systems, platforms must reinitiate verification steps that slow fund movement.

Regulatory alignment plays a role as well. Platforms operating under frameworks from bodies like the European Central Bank and Australia's financial regulators encounter different documentation thresholds. These differences surface during account creation and later affect how overseas remittances clear. Research papers examining multi-jurisdictional payment flows document these coordination gaps in detail.

Examples from Current Operations

Take one e-commerce network serving vendors across Southeast Asia and Europe. Account setup for vendors in high-remittance corridors required additional corporate filings that extended onboarding by several days. Once established, the same vendors experienced fewer transfer rejections because initial compliance checks had already addressed common remittance flags.

Another case involves platforms integrating digital wallets with traditional banking partners. Observers tracking these integrations note that wallet account creation often incorporates remittance routing preferences upfront. This approach reduces later barriers when funds move between continents.

Trends Observed in Mid-2026

By June 2026, several platforms had begun testing unified verification standards that draw from both account establishment and remittance requirements simultaneously. Transaction volume data indicates modest improvements in processing times where these tests occurred. Industry reports highlight ongoing efforts to map common data points between the two processes.

Conclusion

The connections between account establishment routines and overseas remittance barriers shape how effectively web commerce systems handle international payments. Documentation gathered at onboarding directly influences later transfer success rates. Regulatory variations across regions maintain pressure on platforms to refine these linked processes. Continued examination of transaction patterns offers clearer visibility into where adjustments yield measurable reductions in delays.