Encryption Pathways Linking Digital Wallets to Merchant Onboarding in Global Micro-Transaction Ecosystems

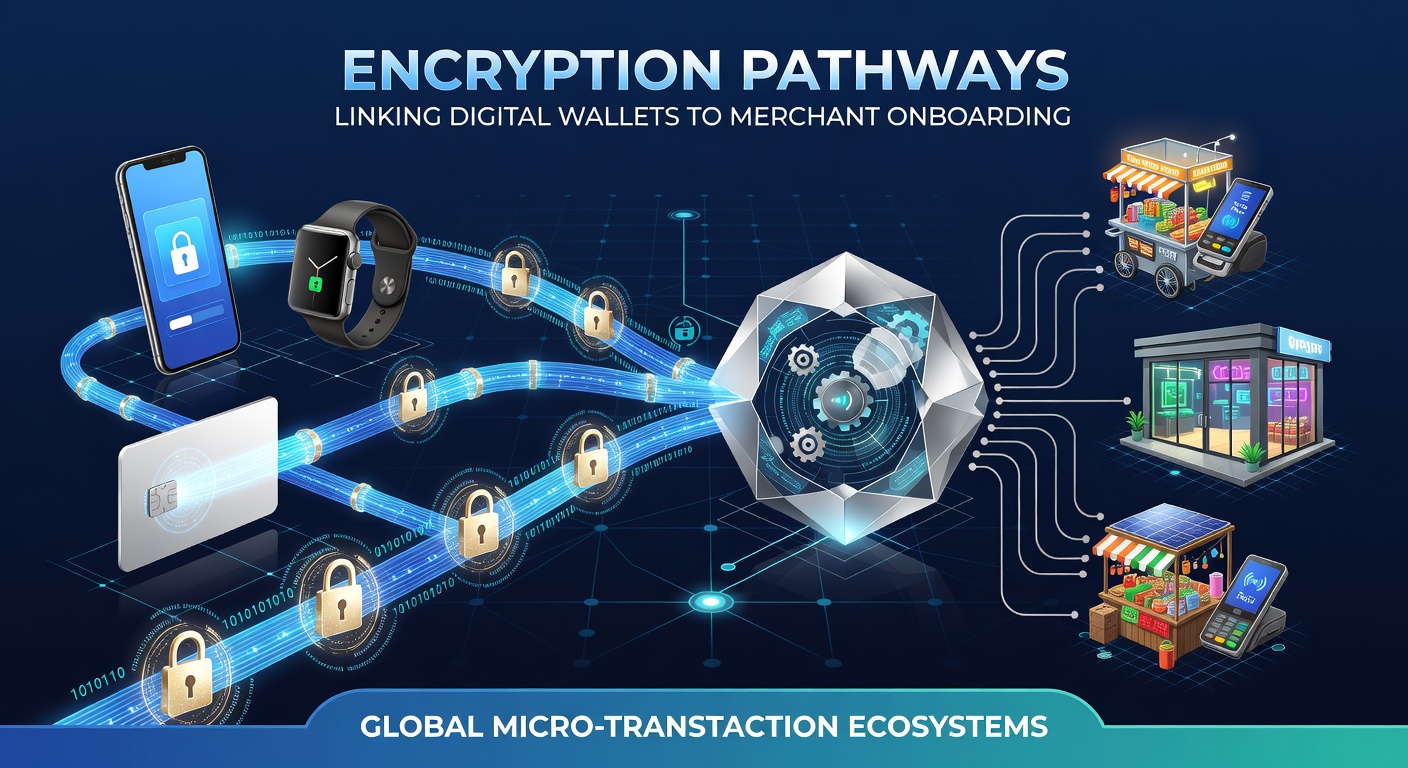

Digital wallets rely on layered encryption protocols to protect transaction data during transfers to merchant accounts, and these same protocols facilitate secure merchant onboarding across international micro-transaction platforms where small-value exchanges occur frequently. Observers note that end-to-end encryption combined with tokenization creates pathways that verify merchant identities while shielding sensitive financial details from interception, and this process operates continuously in ecosystems spanning multiple continents.

Research indicates that public key infrastructure forms the backbone of these pathways because it assigns unique cryptographic keys to each wallet and merchant endpoint, which allows authentication without exposing private data during the initial setup phase. Data from payment networks shows that merchants complete onboarding in under 48 hours when these encryption layers integrate directly with compliance databases, whereas delays often arise from mismatched regional standards for key exchange.

Core Components of Encryption Pathways

Encryption begins at the wallet level with symmetric algorithms such as AES-256 that scramble transaction payloads before they leave the device, and asymmetric methods like RSA handle key distribution between the wallet provider and the merchant's acquiring bank. Those who've examined system architectures know that this dual approach reduces latency in micro-transactions because symmetric keys manage bulk data while asymmetric keys establish trust during onboarding.

Tokenization layers sit atop these foundations by replacing card or account numbers with unique tokens that hold no intrinsic value outside the specific ecosystem, and this substitution occurs automatically once a merchant account receives verification through encrypted channels. Figures reveal that networks processing over 10 billion micro-transactions monthly report fewer than 0.01 percent incidents of token compromise when pathways enforce strict key rotation every 24 hours.

Merchant Onboarding Mechanics

Merchants enter global ecosystems through an encrypted portal that collects business credentials, tax identifiers, and banking details, after which automated systems cross-reference this information against regulatory watchlists using secure multi-party computation. The process advances when the wallet network issues a provisional token to the merchant, which becomes active only after the acquiring institution confirms the encrypted data matches official records.

Studies found that platforms in the Asia-Pacific region complete this verification faster than their European counterparts because they align encryption standards more closely with local banking APIs, and similar patterns emerge in North American markets where standardized protocols reduce manual reviews by 35 percent. As of May 2026, several central banks have begun testing quantum-resistant algorithms within these pathways to prepare for potential future threats to current encryption methods.

Global Ecosystem Integration

Micro-transaction ecosystems span e-commerce platforms, content services, and in-app purchases where values often fall below one dollar, and encryption pathways ensure that each transfer routes through verified merchant accounts without exposing user identities across borders. According to Bank for International Settlements analysis, cross-border micro-transactions grew 22 percent year-over-year in 2025, driven largely by encrypted wallet integrations that bypass traditional card rails.

Regional variations appear in how these pathways handle data residency rules, with some jurisdictions requiring encryption keys to remain within national borders while others permit cloud-based key management under strict audit conditions. Researchers discovered that unified standards from organizations such as the OECD help bridge these differences by outlining baseline requirements for key length, rotation frequency, and audit trails that participating networks adopt voluntarily.

Security Protocols and Compliance

Compliance frameworks mandate that encryption pathways log every key exchange and token issuance without storing plaintext data, which enables regulators to trace anomalies while preserving user privacy. Payment processors implement zero-knowledge proofs in select markets to demonstrate merchant legitimacy without revealing underlying business metrics during onboarding reviews.

One study revealed that ecosystems incorporating hardware security modules at both wallet and merchant endpoints experience 40 percent fewer successful intrusion attempts compared to software-only configurations, and this hardware layer operates independently of the main transaction flow to avoid introducing delays. Observers note that real-time monitoring tools scan these pathways continuously, flagging deviations in encryption patterns that could signal attempted breaches before they affect merchant accounts.

Conclusion

Encryption pathways continue to evolve as the foundation connecting digital wallets with merchant onboarding across global micro-transaction ecosystems, where technical standards and regulatory expectations intersect to support secure small-value exchanges. Data shows sustained growth in adoption rates, and ongoing developments in key management and compliance tools shape how these connections operate in practice.